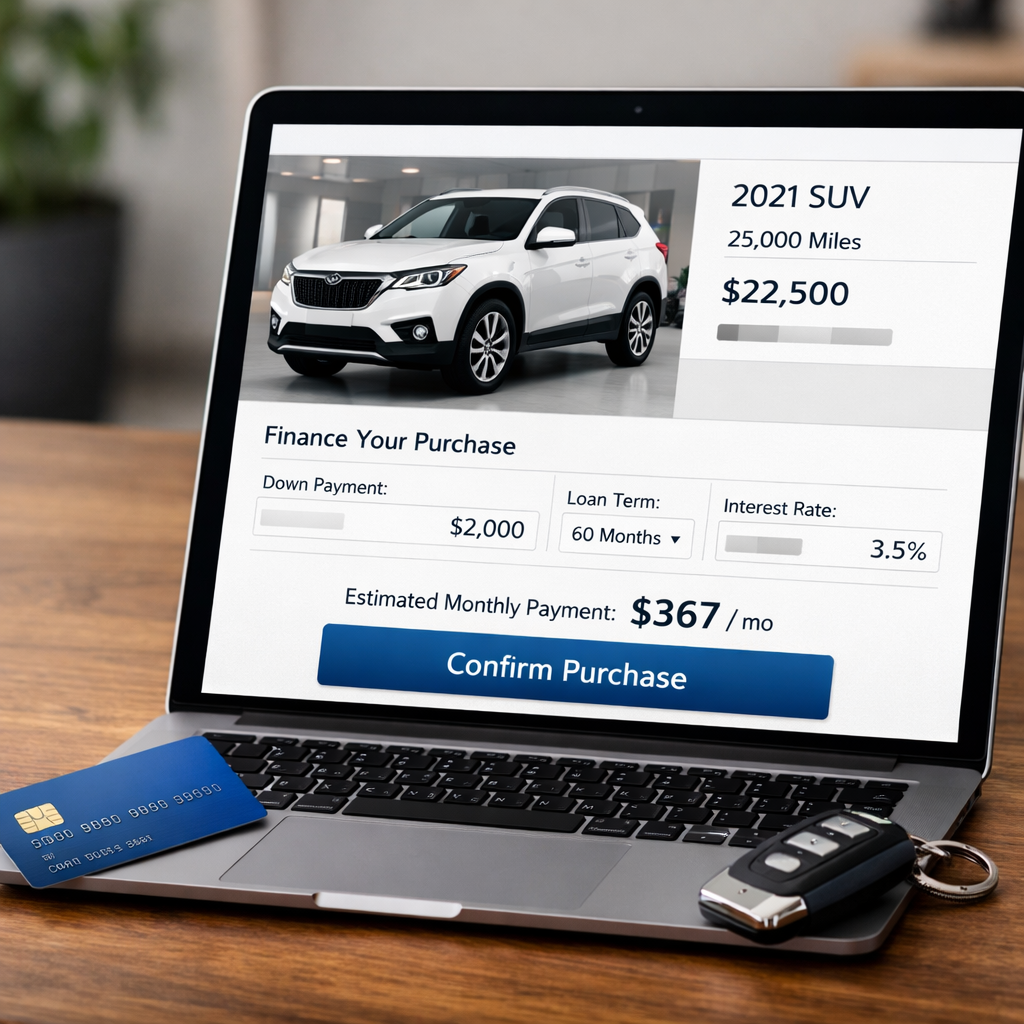

How To Finance And Buy A Car Online In One Step

Buying and financing a car can now happen in a single, seamless online session. The gist: you prequalify with a soft credit check, compare real APRs and terms, pick your vehicle, lock an out-the-door price, e‑sign, and schedule delivery—all without showroom time. Many banks, dealers, and marketplaces support fast approvals and digital contracting, so the “one step” is really one coordinated flow that takes hours instead of days. If you’re asking where to finance and buy a car online in one step, the answer is: on platforms that combine prequalification, transparent pricing, and e‑contracting in one place, backed by your own outside lender quotes for leverage.

What one step really means

One-step online car buying is a streamlined, end‑to‑end journey where you research inventory, get a soft‑credit‑check prequalification, compare lender offers, lock a written out‑the‑door price, e‑sign your loan and purchase documents, and arrange delivery—all in one continuous digital flow. Many platforms enable approvals in minutes with digital paperwork and insurance upload support (see Arizona Financial’s overview of digital car shopping).

Why it matters: shoppers who complete key financing steps online report faster turnarounds and higher satisfaction. In one study, 29% of buyers had already applied for financing online and 96% said they were willing to do so, citing time savings and smoother handoffs between steps (Cox Automotive’s Car Buyer Financing Journey Study).

Car Battery Expert approach

Here’s our cost‑first, lender‑agnostic mini‑map—built around transparency and total cost—for a true one‑step experience:

- Research models that fit your needs and budget.

- Prequalify (soft pull) with multiple sources to get real APR and term ranges.

- Compare offers by total cost (APR + term + fees), not just the payment.

- Lock a written out‑the‑door (OTD) price before any hard inquiry.

- Finalize credit (hard pull), confirming your selected offer and rate lock.

- Validate the vehicle at the VIN level (history + independent inspection).

- E‑sign contracts and schedule delivery or pickup.

Consumer protections: get outside quotes from your bank/credit union and at least one online marketplace to reduce dealer finance markups, then choose the lowest total interest, not the lowest monthly payment (Forbes’ guide to online car‑buying sites). Use Car Battery Expert calculators and used‑car pricing guides to sanity‑check OTD and value (see our tools at Car Battery Expert).

Prepare your budget and documents

Have these ready to speed underwriting and avoid back‑and‑forth:

- Recent pay stubs and employer info

- Proof of residence (utility bill or lease)

- Driver’s license

- Current insurance (or plan to bind before delivery)

- Trade‑in title/loan details (if applicable)

- Your estimated OTD budget (vehicle price + taxes + title/registration + documentation + dealer fees + any delivery)

Out‑the‑door (OTD) price is the full amount you’ll pay to take the car home, inclusive of taxes and fees—use it for apples‑to‑apples comparisons.

Affordability rule of thumb: aim for a payment that keeps total car costs (loan, insurance, fuel/EV charging, maintenance) around 10–15% of take‑home pay. Pre‑calculate a monthly range and down payment target. When you’re ready to finalize, cluster hard inquiries within a 14–45 day rate‑shopping window so they’re treated as one for scoring. Car Battery Expert calculators can help you set a clear monthly range and OTD target before you apply.

Get instant, soft-credit-check prequalifications

Prequalification is a soft‑credit‑check estimate of your likely APR, term options, and maximum loan amount based on limited credit data. It doesn’t affect your score and helps you set a realistic budget before any hard inquiry. Many banks and marketplaces now show real prequalified ranges online (see Chase Auto’s online finance experience).

Where to prequalify first:

- Before you shop offers, model payments and total interest with Car Battery Expert calculators so you know your target range.

- Your bank or local credit union: establishes a personal benchmark and often competitive rates.

- At least one online marketplace that returns multiple offers within minutes to compare side‑by‑side (e.g., platforms highlighted by Arizona Financial and marketplaces like Automatic).

Quick comparison template (fill this out as offers arrive):

| Lender type | What you see at prequal | Term options | Method | Rate‑lock (if any) |

|---|---|---|---|---|

| Bank/Credit union | Personalized APR range | Common choices offered | Soft pull online | Varies by lender |

| Online bank | Estimated APR + payment range | Multiple term lengths | Soft pull online | Varies by lender |

| Marketplace platform | Multiple lender offers at once | Multiple per offer | One soft pull | Often stated per offer |

Tip: Some banks allow online approval with a 30‑day lock once you finalize (see Chase Auto).

Compare offers from banks, credit unions, and online lenders

Compare apples to apples. Focus on total interest paid and fees—not just the monthly number.

Recommended comparison table (example for illustration):

| Offer | APR | Term (months) | Est. total interest on $30,000 | Fees (origination, GAP/ancillaries) | Rate lock | Prepayment policy |

|---|---|---|---|---|---|---|

| A | 6.49% | 60 | ~$5,200 | $0 orig.; optional GAP/warranty | 30 days | No penalty |

| B | 5.99% | 72 | ~$5,770 | $0 orig.; add‑ons offered | 30 days | No penalty |

| C | 7.19% | 48 | ~$4,450 | $150 orig.; no add‑ons bundled | 15 days | No penalty |

- Remember: the lowest payment can cost more overall if the term is stretched—prioritize the lowest total interest.

- Negotiation leverage: bring third‑party preapprovals to the dealer; let them try to beat your best rate, then pick the lowest total cost (Forbes).

- Proof it works: buyers who completed key finance steps online saved time and reported higher satisfaction at the store (Cox Automotive study).

Pick your car and validate price with VIN data

Browse dealer and marketplace inventory, filter by trim/specs, and review transparent pricing and vehicle history where shown (Arizona Financial notes platforms with integrated research and transparency).

Before you commit on a used car:

- Pull a VIN‑based vehicle history report; start with NMVTIS data.

- Book an independent pre‑purchase inspection—even if buying from a dealer (Forbes).

- Mini‑checklist: history flags (title/odometer/accident), comparable listings, reconditioning receipts, warranty status, freight or add‑on scrutiny.

Car Battery Expert used‑car pricing guides can help you benchmark fair value and spot mismatched add‑ons before you agree to an OTD price.

Lock the out-the-door price

Negotiate by phone or email and secure a written OTD quote before any hard credit application (Consumer Reports’ online‑buying guidance).

Use this line‑item template:

- Vehicle price (VIN‑specific)

- Taxes

- Title/registration

- Documentation fee

- Dealer‑installed options

- Add‑ons (GAP, service contract, accessories)

- Delivery/shipping fee (if applicable)

Many online retail tools support remote price transparency and delivery scheduling—use that to avoid last‑minute surprises (Arizona Financial).

Finalize credit, e-sign, and arrange delivery

- Submit the final credit application to lock your chosen rate/term; some lenders approve online and provide a 30‑day lock once approved (Chase Auto).

- Complete digital paperwork and e‑contracting—modern dealer tools enable starting and signing deals remotely (Cox Automotive’s digital retailing strategies).

- Upload proof of insurance and schedule home delivery or express pickup where available (Arizona Financial).

Hybrid is normal: about 75% who start online prefer to continue in‑store on a tablet—just ensure no duplicate data entry to keep satisfaction high (Cox Automotive digital strategies).

Safeguards to avoid costly mistakes

- After you lock OTD, compare dealer financing with outside offers—choose by total cost to avoid payment packing, extended terms, or unnecessary add‑ons (Forbes).

- For used cars, require both a VIN‑based history report and an independent inspection before funding.

- Tech can help: integrated marketplaces and emerging AI assistants can streamline comparisons and scheduling, but you should still verify disclosures, fees, and contract terms carefully (see Automatic’s marketplace model and Capital One’s take on AI in auto retail).

- If you later find a lower rate, you can refinance—just weigh fees and the remaining term.

Frequently asked questions

Can I really finance and buy a car online in one step?

Yes—many platforms let you prequalify, compare offers, lock an out‑the‑door price, e‑sign, and schedule delivery in a single digital flow, with a final credit check and quick verifications before funding. Car Battery Expert helps you plan the steps and total cost so you move through that flow with fewer surprises.

Will prequalification hurt my credit score?

No. Prequalification uses a soft credit check that doesn’t affect your score; only the final application triggers a hard inquiry. Use Car Battery Expert to model a budget with your prequal ranges before you proceed.

Is bank or dealer financing better for an online purchase?

Bank or credit union preapproval often provides lower, more transparent rates; share it and let the dealer try to beat it, then choose the lowest total cost. Car Battery Expert tools make it easy to compare total interest and fees side‑by‑side.

How do I verify a used car’s price before I commit?

Pull a VIN‑based history report, compare similar listings, and order an independent inspection to validate price and negotiate any reconditioning credits. Car Battery Expert pricing guides help you sanity‑check OTD against fair‑market value.

What fees are included in the out-the-door price?

OTD includes the vehicle price plus taxes, title/registration, documentation fees, dealer add‑ons, and any delivery charges—always get it in writing before signing. Compare the written quote to your Car Battery Expert budget to confirm it fits.